Florida Legislature Proposes Not to Conform to One Big Beautiful Bill Tax Relief Provisions

On February 24, the Florida House and Senate released their initial tax proposals for the 2026 Regular Session. Both initial bills decouple from the corporate tax relief provisions contained in Trump’s One Big Beautiful Bill Act, although in different methods.

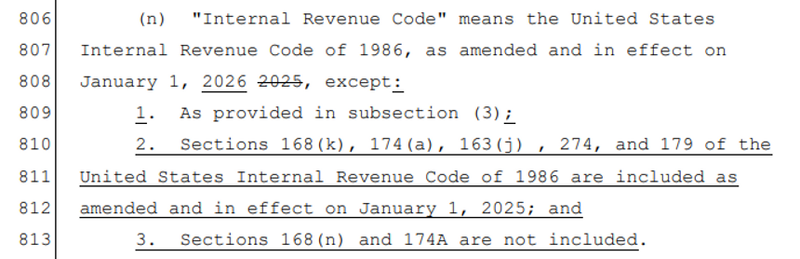

House Bill 7031 from the Ways and Means Committee includes corporate income conformity tax provisions in Sections 23-25. While the House bill updates the January 1, 2026, version of the Internal Revenue Code, it then excepts all the One Big Beautiful (OB3) provisions:

Senate Bill 7048 also updates the Florida corporate income tax code to January 1, 2026, then provides specific decoupling for each of the federal provisions:

The 2026 Florida Regular Session is scheduled to conclude March 13, 2026.

While the House bill updates the January 1, 2026 version of the Internal Revenue Code, it then excepts all the One Big Beautiful (OB3) provisions

-

- name

- H. French Brown, IV

- title

- Partner

- phones

- D: 850.214.5075

- fbrown@joneswalker.com